Nov 15, 2019

A month after the new year begins, your business may be required to comply with rules to report amounts paid to independent contractors, vendors and others. You may have to send 1099-MISC forms to those whom you pay nonemployee compensation, as well as file copies with the IRS. This task can be time consuming and there are penalties for not complying, so it’s a good idea to begin gathering information early to help ensure smooth filing.

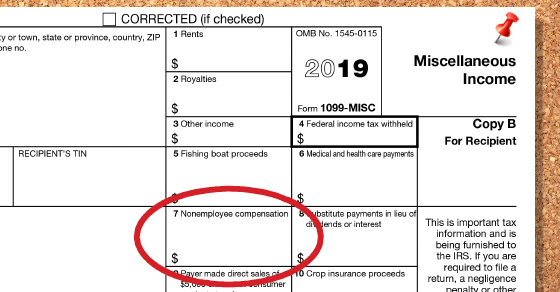

Deadline

There are many types of 1099 forms. For example, 1099-INT is sent out to report interest income and 1099-B is used to report broker transactions and barter exchanges. Employers must provide a Form 1099-MISC for nonemployee compensation by January 31, 2020, to each noncorporate service provider who was paid at least $600 for services during 2019. (1099-MISC forms generally don’t have to be provided to corporate service providers, although there are exceptions.)

A copy of each Form 1099-MISC with payments listed in box 7 must also be filed with the IRS by January 31. “Copy A” is filed with the IRS and “Copy B” is sent to each recipient.

There are no longer any extensions for filing Form 1099-MISC late and there are penalties for late filers. The returns will be considered timely filed if postmarked on or before the due date.

A few years ago, the deadlines for some of these forms were later. But the earlier January 31 deadline for 1099-MISC was put in place to give the IRS more time to spot errors on tax returns. In addition, it makes it easier for the IRS to verify the legitimacy of returns and properly issue refunds to taxpayers who are eligible to receive them.

Gathering information

Hopefully, you’ve collected W-9 forms from independent contractors to whom you paid $600 or more this year. The information on W-9s can be used to help compile the information you need to send 1099-MISC forms to recipients and file them with the IRS. Here’s a link to the Form W-9 if you need to request contractors and vendors to fill it out: target=”_blank”>https://bit.ly/2NQvJ5O.

Form changes coming next year

In addition to payments to independent contractors and vendors, 1099-MISC forms are used to report other types of payments. As described above, Form 1099-MISC is filed to report nonemployment compensation (NEC) in box 7. There may be separate deadlines that report compensation in other boxes on the form. In other words, you may have to file some 1099-MISC forms earlier than others. But in 2020, the IRS will be requiring “Form 1099-NEC” to end confusion and complications for taxpayers. This new form will be used to report 2020 nonemployee compensation by February 1, 2021.

Help with compliance

But for nonemployee compensation for 2019, your business will still use Form 1099-MISC. If you have questions about your reporting requirements, contact us.

© 2019

Nov 13, 2019

Most businesses report financial performance using U.S. Generally Accepted Accounting Principles (GAAP). But the income-tax-basis format can save time and money for some private companies. Here’s information to help you choose the financial reporting framework that will work for your situation.

The basics

GAAP is the most common financial reporting standard in the United States. The Securities and Exchange Commission (SEC) requires public companies to follow it — they don’t have a choice. Many lenders expect large private borrowers to follow suit, because GAAP is familiar and consistent.

However, compliance with GAAP can be time-consuming and costly, depending on the level of assurance provided in the financial statements. So, some private companies opt to report financial statements using an “other comprehensive basis of accounting” (OCBOA) method. The most common OCBOA method is the tax-basis format.

Key differences

Departing from GAAP can result in significant differences in financial results. Why? GAAP is based on the principle of conservatism, which prevents companies from overstating profits and asset values. This runs contrary to what the IRS expects from for-profit businesses. Tax laws generally tend to favor accelerated gross income recognition and won’t allow taxpayers to deduct expenses until the amounts are known and other deductibility requirements have been met. So, reported profits tend to be higher under tax-basis methods than under GAAP.

There are also differences in terminology. Under GAAP, companies report revenues, expenses and net income. Conversely, tax-basis entities report gross income, deductions and taxable income. Their nontaxable items typically appear as separate line items or are disclosed in a footnote.

Capitalization and depreciation of fixed assets is another noteworthy difference. Under GAAP, the cost of a fixed asset (less its salvage value) is capitalized and systematically depreciated over its useful life. For tax purposes, fixed assets are depreciated under the Modified Accelerated Cost Recovery System (MACRS), which generally results in shorter lives than under GAAP. Salvage value isn’t subtracted for tax purposes, but Section 179 and bonus depreciation are subtracted before computing MACRS deductions.

Other reporting differences exist for inventory, pensions, leases, start-up costs and accounting for changes and errors. In addition, companies record allowances for bad debts, sales returns, inventory obsolescence and asset impairment under GAAP. But these allowances generally aren’t permitted under tax law.

Departing from GAAP

GAAP has become increasingly complex in recent years. So some companies would prefer tax-basis reporting, if it’s appropriate for financial statement users.

For example, tax-basis financials might work for a business that’s owned, operated and financed by individuals closely involved in day-to-day operations who understand its financial position. But GAAP statements typically work better if the company has unsecured debt or numerous shareholders who own minority interests. Likewise, prospective buyers may prefer to perform due diligence on GAAP financial statements — or they may be public companies that are required to follow GAAP.

Contact us

Tax-basis reporting makes sense for certain types of businesses. But for other businesses, tax-basis financial statements may result in missing or even misleading information. We can help you evaluate the pros and cons and choose the appropriate reporting framework for your situation.

© 2019

Nov 11, 2019

In many industries, market conditions move fast. Businesses that don’t have their ears to the ground can quickly get left behind. That’s just one reason why some of today’s savviest companies are establishing so-called “shadow” (or “mirror”) boards composed of younger, nonexecutive employees who are on the front lines of changing tastes and lifestyles.

Generational change

Millennials — people who were born between approximately 1981 and 1996 — have been flooding the workplace for years now. Following close behind them is Generation Z, those born around the Millennium and now coming of age a couple of decades later.

Despite this influx of younger minds and ideas, many businesses are still run solely by older boards of directors that, while packed with experience and wisdom, might not stay closely attuned to the latest demographic-driven developments in hiring, product or service development, technology, and marketing.

A shadow board of young employees that meets regularly with the actual board (or management team) can help you overcome this hurdle. Ideally, the two boards mentor each other. The older generation shares their hard-earned lessons on leadership, governance, professionalism and the like, while the younger employees keep the senior board abreast of the latest trends, concerns and communication tools among their cohort.

Other benefits

You also can tap the shadow board for their input on issues that directly affect them. For example, would they welcome a new employee benefit under consideration or regard it as irrelevant? Similarly, you can use the board to “test drive” strategies targeting their generation before you get too far down the road.

And your shadow board can serve as generator of new initiatives and innovations, both employee- and customer-facing. Some companies with shadow boards have ended up overhauling their processes, procedures and even business models based on ideas that first emerged from the younger employees’ input.

Another benefit? Shadow boards can keep traditionally job-hopping Millennials from jumping ship. Many are eager to get ahead, often before they’re equipped to do so, and they don’t hesitate to look elsewhere. Selecting younger employees for a shadow board sends them the message that you see their potential and are invested in grooming them for bigger and better things. It also facilitates succession planning, a practice too many businesses overlook.

The right approach

Don’t establish a shadow board just for appearances or without true commitment. That can do more harm than good. Younger generations see lip service for what it is, and word will spread fast if you’re ignoring the shadow board or refusing to seriously consider its input. When done right, this innovative effort can pay off in the long run for everyone involved. Our firm can help you further explore the financial and strategic feasibility of the idea.

© 2019

Nov 6, 2019

Technology is altering the traditional approach to internal audits. Instead of reviewing reams of paperwork, today’s auditor is learning to use electronic records. In turn, going paperless facilitates a concept known as “continuous auditing,” where internal auditors continually gather data to support their procedures. Here’s how your business can modernize this process.

Targeting specific areas

Not every functional area of your company lends itself to paperless and continuous auditing. To determine whether sufficient, timely and accurate electronic data exists, you’ll need to review the systems that store and generate your company’s data.

For example, if a portion of your inventory accounting processes still relies on paper, it may not present an ideal candidate for paperless and continuous auditing. Alternatively, if your accounts payable (AP) process functions entirely on electronic records, it’s logical to include AP in the continuous audit program.

Planning the program

Before you can adopt a continuous audit program, you must determine:

- Your primary and secondary business goals, and

- The key risks you hope to mitigate.

Then you can design your program accordingly. For example, if you plan to continuously audit the AP process and you’re concerned about occupational fraud, you may decide to put a rule in place that looks for the creation of vendors whose address matches that of an employee.

From a practical perspective, it’s important to document how often you plan to sample the data that the continuous audit program makes available. Keep in mind that a daily review of the output often generates the greatest benefit.

Ensuring accountability

To help ensure accountability, a process must exist to review and evaluate the audit output. For example, if the review of employee payroll data uncovers unusual payroll disbursements, a process must exist to investigate those discrepancies.

The individual who should be responsible for reviewing the data will depend on the size and structure of your company. It could fall to the internal audit department, someone within the fraud team or a department manager.

Time for change?

Robust internal audits help management correct operational issues quickly, which prevents money from being wasted and risks from spiraling out of control. If implemented correctly, paperless and continuous auditing can improve your company’s internal audit and oversight abilities while also reducing its costs. Contact us for help converting paper records to an electronic format, as well as planning and implementing a continuous internal audit program that targets the optimal areas of your business operations.

© 2019

Nov 4, 2019

Accounting software typically sells itself as much more than simple spreadsheet or ledger. The products tend to pride themselves on being comprehensive accounting information systems — depending on the price point, of course.

So, is your accounting software living up to the hype? If not, there are a couple of relatively simple steps you can take to improve matters.

Train and retrain

Many businesses grow frustrated with their accounting software packages because they haven’t invested enough time to learn their full functionality. When your personnel are truly up to speed, it’s much easier for them to standardize reports to meet your company’s needs without modification. Doing so not only reduces input errors, but also provides helpful financial information at any point during the year — not just at month end.

Along the same lines, your company should be able to perform standard journal entries and payroll allocations automatically within your accounting software. Many systems can recall transactions and automate, for example, payroll allocations to various programs or vacation accrual reports. If you’re struggling to extract and use these types of financial information, you might be underusing your accounting software (or it might be time for an upgrade).

Ideally, a champion on your staff may be able to step up and share his or her knowledge with others to get them up to speed. Otherwise, you could explore the cost of engaging an external consultant to review your software’s functionality and retrain staff on its basic features, as well as the many shortcuts and advanced features available.

Commit to continuous improvement

Accounting systems that aren’t monitored can become inefficient over time. Encourage employees to be on the lookout for labor-intensive steps that could be better automated, along with processes that don’t add value and might be eliminated. Also, note any unusual activity and look for transactions being improperly reported — remember the old technological adage, “garbage in, garbage out.”

Leadership plays an important role, too. Ownership and management are ultimately responsible for your company’s overall financial oversight. Periodically review critical documents such as monthly bank statements, financial statements and accounting entries. Look for vague items, errors or anomalies and then determine whether misuse of your accounting system may be to blame.

Take the time

Many businesses don’t even realize they have a problem with their accounting software until they take the time to evaluate and improve it. And only then does the system finally deliver on the hype — sometimes. Our firm can help you review your accounting software and ensure it’s delivering the information you need to make good business decisions.

© 2019

Recent Comments